カリフォルニア州 キャンベル、2011年6月14日 市場調査会社Infonetics Researchは今日 Shira LevineによるConvergent Charging Software and Services market share and forecast report 抜粋をリリースした。

アナリストノート

“事業者は既存のINベースプリペイド システムや分割払いシステムなどの請求システムによってさまざまな制約を受けている。 統合課金は全面的な請求システム変更プロジェクトの実行を要することなく事業者が顧客への新しいサービスや価格設定モデルを紹介することができる一つの方法だ。それに統合課金の導入は緩やかなシステム切り替えプロジェクトの第一歩にもなりえる。 統合課金の初期成長は主に東南アジア、インドそして東ヨーロッパなどの新興市場で見られたが、最近ではより成熟した西ヨーロッパなどの市場でも初期投資が見られるようになった,"と Infonetics Research 新世代OSSとポリシー担当主任アナリスト Shira Levineは指摘する。

本リポートは、多様なサービス媒体(音声、動画、データ)、ネットワークタイプ(有線、無線)、そして地域を超越してプリペイド、ポストペイド、ハイブリッド・プリペイド/ポストペイ・など多数の決済方による処理を可能する統合課金のサービス内容(コンサルティング、インテグレーション、ホスト/マネージサービスなど)と統合課金ソフトフェアをより深く検討し、 急成長を見せる統合課金マーケットについて業界内で最も包括的な内容を提供している。

統合課金マーケットのハイライト

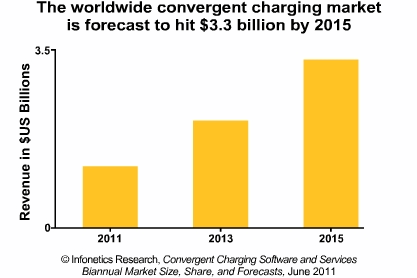

- 世界的な統合課金マーケットはソフトフェアとサービスを含め2009年から2010年にかけ37%(8億6230万ドル)成長し、 Infoneticsは2015年には33億ドルまで成長するだろうと予測する。

- 2010年にTelcordiaがわずかにComverseを抜いてはいるが、 現在Telcordia and Comverse が総合的な統合課金マーケットで事実上の首位として互角の勝負をしている 。 Ericsson とHuaweiが3位と4位に続いている。

- スマートメーターとユーティリティー間、あるいはテレマティクスデバイスとフリート管理システム間のような機器間(M2M)取り引きが、いすれはモバイルネットワークにおける人間による支払処理容量を遥かに超えるため、新しい支払処理容量の水準とそれに対応できる請求ソリューションの必要性に迫られるだろう。

- 職員用ハイブリッド口座、クラウドサービスの収益決済、機器間取り引きのリアルタイム管理をサポートする 統合課金ソリューションに関心が集まっている。

- 顧客が携帯で支払が出来るサービスを提供する事業者の出現など、いまや携帯マネーは拡大しつつある現象だ。 例としては個人の預金残高範囲で小額からの購入も可能なOi Brazil、そして "お財布携帯"として知られる 日本の NTT DoCoMoが提供するサービスは携帯端末を銀行と連結し、携帯を個人が保有しているクレジットカードの代用として使用できる。

- 今後は時間帯や契約者の場所によって事業者がより柔軟な価格提供をすることができる総合ポリシー/課金ソリューションの必要性が高まるだろう、またこのトレンドはベンダー間のM&Aアクティビティを継続させることとなるだろう。

- 統合課金可能なのは主に無線によるものだが、いくつかの有線事業者は multi-service convergence の導入に向けて試験を開始している。 例としは携帯機能を付帯した quad-playを提供するケーブル事業者やIPTV契約者にプリペイド ビデオ・オン・デマンドコンテンツへのアクセスを提供する有線ブロードバンド事業者、そして自社のクラウド戦略に新たに統合課金の機能をを融合させたサポートを提供する固定通信事業者などだ。

Infonetics' biannual Convergent Charging Software and Services report provides worldwide market share, worldwide and regional market size, in-depth analysis, and forecasts through 2015 for convergent charging software and services.

Vendors tracked include Accenture, Acision, Alcatel-Lucent, Amdocs, Atos Origin, CapGemini, Cerillion, Comptel, Comverse, Convergys, Datatronics, Ericsson, Formula Telecom Solutions, Hewlett-Packard, Huawei, IBM, Intec, Logica CMG, Nokia Siemens, Openet, Oracle, Orga, Redknee, SAP, Tata, Tech Mahindra, Telcordia, TietoEnator, Volubill, ZTE, and others.

The report includes customer wins and service provider/vendor announcements by region and date, including activity between vendors and global operators such as life, Loop Mobile, March Communications, Meteor Mobile Communications, Movistar Venezuela, P&T Luxembourg, LUXGSM, Smart Communications, Tunisiana, Vodacom Tanzania, and Zain Kuwait.

(原文)

Strong convergent charging market driven by payment flexibility, service innovation

Campbell, CALIFORNIA, June 14, 2011—Market research firm Infonetics Research today released excerpts from its June Convergent Charging Software and Services market share and forecast report, led by analyst Shira Levine..

ANALYST NOTE

"Operators are constrained by their existing billing systems, both IN-based prepaid systems and batch billing systems for the postpaid market. Convergent charging represents a way for operators to deliver new services and offer new pricing models without embarking on full-scale billing transformation projects, and can actually be the first step in a gradual migration project. While initial growth in convergent charging has been in emerging markets such as Southeast Asia, India and eastern Europe, we're seeing early investment in more mature markets, including western Europe," notes Shira Levine, directing analyst for next gen OSS and policy at Infonetics Research.

The report is the industry's most comprehensive report on the emerging convergent charging market, taking an in-depth look at convergent charging services (consulting, integration, hosted/managed services) and convergent charging software that can handle multiple payment methods, such as prepaid, postpaid and hybrid prepay/postpaid models, across service types (voice, video, data), network types (wireline, wireless), and regions.

CONVERGENT CHARGING MARKET HIGHLIGHTS

- The global convergent charging market, including software and services, grew 37% in 2010 over 2009 to $862.3 million, and is forecast by Infonetics to grow to $3.3 billion in 2015

- Telcordia and Comverse are now neck and neck in the overall convergent charging market, with Telcordia slightly edging past Comverse in 2010; Ericsson and Huawei are 3rd and 4th

- Machine-to-machine (M2M) transactions, such as between smart meters and utilities, and between telematics devices and fleet management systems, will far exceed human transactions on the mobile network, driving the need for charging solutions that can account for and reconcile that level of transaction volume

- There is interest in convergent charging solutions that support enterprise services, such as hybrid accounts for employees, revenue settlement for cloud services, and real-time management of M2M transactions

- Mobile money is a growing phenomenon, with some operators enabling subscribers to use their cell phones to make payments, such as Oi Brazil, which allows users to pay for small purchases from their prepaid balance, and NTT DoCoMo in Japan, which offers a "mobile wallet" service in conjunction with banks, where the mobile phone replaces a subscriber's existing credit card

- There will be increasing demand for integrated policy/charging solutions that enable operators to offer more flexible pricing models, such as variable pricing based on time of day or the subscriber's location; this trend will drive continued M&A activity between vendors

- Though the convergent charging opportunity is primarily a wireless one, some wireline operators are experimenting with multi-service convergence, including cable operators delivering quad-play with added mobile capabilities, wireline broadband operators offering their IPTV subscribers access to prepaid video-on-demand content, and fixed line operators supporting their cloud strategies with convergent charging capabilities