2011年9月16日、英国ロンドン発――テクノロジー市場調査会社Infonetics Researchは今日、『Residential Femtocell Services: Global Service Provider Survey (仮訳:家庭向けフェムトセル・サービス:サービス・プロバイダの世界調査)』の抜粋版を発表した。抜粋版の元となった報告書は、フェムトセル・サービス関連各社のニーズを探り、フェムトセル・ネットワーク装置市場の動向を分析するために、フェムトセル・サービスを既に開始しているか、2012年までに開始する予定のキャリア各社に、聞き取り調査を行って作成したものである。

アナリストノート

「当社が行った2011年のフェムトセル調査の結果を見れば、家庭向けフェムトセル市場は、フェムトセル技術のより高度な応用へと進化することが分かりますが、来年は、ほとんどの通信事業社がその初期段階にしか至れない模様です。フェムトセルは、本格的な家庭向けモバイル・ネットワークの中央ハブとして期待されていますが、その道のりは実に長いシナリオです。短期的には、既存のモバイル体験を改善すること (音声カバレッジと一貫したデータ・スループットを実現すること) が消費者の期待する重要課題です。」とInfonetics Research社でマイクロ波とスモールセルを担当する主席アナリストRichard Webb (リチャード・ウェブ) 氏は述べる。

家庭向けフェムトセル調査のハイライト

- 2012年まで、フェムト機能を後付けして市場に出回るサービスおよびアプリケーションでもっとも顕著なのは、バーチャル・ホームフォン番号とメディア・ファイルの共有である。

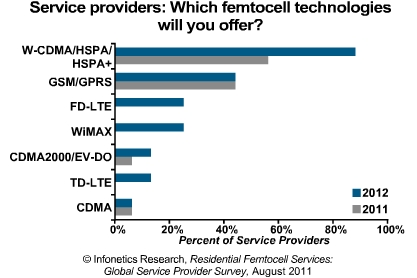

- 現在も2012年中も3GPPフェムトセルが優勢の見込み。牽引役はW-CDMA/HSPA装置である。

- フェムトセルをベースにFD-LTE (周波数分割複信(FDD) を利用したLTE) やWiMAXを提供する通信事業社の数は2012年までに0から25%に成長する。どちらの技術においても、商用化されたフェムトセル・ソリューションがまだ存在しないことを鑑みると、非常に大きな成長が予想されていると言える。

- 通信事業各社にとってもっとも重要なフェムトセルの性能は、ラジオ・カバレッジだが、もちろんその後は低価格化である。その理由は、消費者売り上げは一般に量が出ないと始まらないため、適切な価格設定はどのCPEセグメントにとっても死活問題だからである。

- フェムト技術を組み込んだDSLやケーブル・ブロードバンド・ルータ/ゲートウェイなど、統合フェムトセルCPE分野では、大きな成長が見込まれている。

- 主として、通信事業者は現在、フェムトセルをまずは1回限りか月払いのサービスとして提供しているが、いずれはスマートフォンかタブレットとネットブックと一緒にパッケージ化するか、あるいは、一部の優良ユーザないしは一部のデバイスに放出しようと考えている会社は多い。

Infoneticsが2011年8月に発行した全21ページの報告書『Residential Femtocell Services survey (仮訳:家庭向けフェムトセル・サービス調査)』には、現在、提供中か計画中のフェムトセル技術、フェムトセル・サービスの特徴、付加サービス、マーケティング・広告戦略販売戦略、CPE性能、販売促進の鍵、フォーム・ファクター、フェムトセル・サービスの見込み収入、ARPU、フェムトセル加入者数などを尋ねたキャリアへの聞き取り調査結果とその分析が収められている。

Infoneticsのフェムトセル調査は、すでにフェムトセル・サービスを開始したサービス・プロバイダ、あるいは2012年までに開始するサービス・プロバイダへの聞き取り調査を基盤としている。これらのキャリアは、全部で世界のテレコム収入の実に23%、テレコムCAPEXの22%にも上り、その内訳は、ヨーロッパ、北米、アジア・太平洋地域の既存業者、モバイル通信業社、競合通信業社、ケーブル通信業社と、多岐に亘る。現在までのところ、すでにフェムトセル・サービスを開始したモバイル通信事業社は31社、今後開始するとしている会社は43社である。このことから、Infoneticsの調査サンプル16社は通信事業市場の約25%に相当すると考えられる。

(原文)

Femtocell operator survey provides glimpse into the future of femtocell services

London, UK, September 16, 2011—Technology market research firm Infonetics Research today released excerpts from its Residential Femtocell Services: Global Service Provider Survey, for which carriers that have launched femtocell services or plan to by 2012 were interviewed to assess their needs and to analyze trends in the femtocell network equipment market.

ANALYST NOTE

"Our 2011 femtocell survey results indicate a roadmap for the evolution of the residential femtocell market toward more sophisticated usage of femtocell technology, but most operators will only be in the early phase of this journey over the next year. The femtocell as the central hub of a fully fledged mobile home network is very much a long-term scenario. In the short term, improving the existing mobile experience (namely voice coverage and consistent data throughput) is the key femto goal in the consumer space," notes Richard Webb, directing analyst for microwave and small cells at Infonetics Research.

RESIDENTIAL FEMTOCELL SURVEY HIGHLIGHTS

- The most prominent bolt-on femto-enabled services and applications coming to market by 2012 are virtual home phone numbers and media file sharing

- 3GPP femtocells dominate the residential market now and in 2012, with W-CDMA/HSPA devices leading the charge

- The number of operators offering FD-LTE (LTE using frequency division duplexing) and WiMAX based femtocells grows from zero to 25% by 2012, significant expected growth considering neither technology has a commercially available femtocell solution yet

- Radio coverage is the most important femtocell feature for operators, of course, followed by pricing, as pricing is a vital criterion in any CPE segment because consumer sales are usually volume driven

- Significant growth is expected in integrated femtocell CPE, such as DSL or cable broadband routers and gateways with embedded femto technology

- Predominantly, operators currently offer femtocells as a one-off purchase or with a monthly outlay, but many expect to eventually bundle them with smartphones or tablets and netbooks or to give them away to select users or with select devices

Infonetics’ August 2011 21-page Residential Femtocell Services survey report includes analysis and carrier responses to questions about current and future femtocell technologies offered, service features, add-on services, marketing and advertising strategies, sales strategies, CPE features, purchase drivers, form factors, expected femtocell service revenue, ARPU, and femtocell subscribers.

Infonetics’ femtocell survey is based on interviews with purchase-decision makers at service providers that have launched femtocell services or plan to by 2012. Together, the carriers represent a significant 23% of worldwide telecom revenue and 22% of telecom capex and are a mix of incumbents, mobile operators, competitive operators, and cable operators from Europe, North America, and Asia Pacific. To date, only 31 mobile operators have launched commercial femtocell services, with another 43 committing to do so; in this context Infonetics’ survey sample (16) represents close to 25% of the operator market.