カリフォルニア州キャンベル-2011年12月1日-市場調査会社Infonetics Researchが、ベンダーの市場占有率、市場予測、そしてLTE及びWIMAX展開を含むモバイル及びワイヤレス装置市場を一望した、2011年第3四半期(3Q11)の2G/3G/4G (LTE 及びWiMAX)インフラ及び加入者レポートからの抜粋を本日リリースした。

アナリストノート

「多くの人々は、欧州金融危機の只中で見落としているのではないでしょうか?EUの『ビッグ5』電気通信事業者-- Deutsche Telekom、France Telecom、Telecom Italia、Telefonica, Vodafone -には、合計すれば現金で100億以上の豊かな資金力があるのですよ!」Infonetics Researchのモバイル・インフラ担当主要アナリストStephane Teralは指摘する。「ええ、確かに困難な状況ではあり、多くの通信業社が、特にヨーロッパと中東においては、新たな収益を生み出すのには困難な時期にありますが、しかし電気通信業界が崩壊した訳ではないという事実は依然として変わりありません。市場基盤は変わっていません。サービスプロバイダが容赦なく増大するトラフィックを管理する為には、ネットワークをアップグレードし続けなければなりません。その結果として我々は、この危機による電気通信に対する影響は、全体的には微小なものであり続けるという見解を維持します」

「確かに、第3四半期における2G/3G/4Gモバイル・インフラ市場全体は、ベンダーが季節要因(第3四半期は過去5年のうち4年で低下している)の為と説明するであろう連続的低下を見ましたが、この市場は1年前の四半期からほぼ9%上昇しています。未来への指針となるのは、1年前から330%上昇したLTE装置部門です。Verizonの LTEが出費のピークを過ぎた今、AT&Tと他の全世界の事業者に加えて、現行システムの増強に見切りをつけたSprintによってリードされる『LTE 第二波』が始まっています。これらの活動の結びつきが、LTEへの移行を速めるのを助け、我々のLTE予測を強化するように促しているのです」

Infonetics Researchのマイクロウェーブ及びスモールセル担当アナリスト兼、本レポート共同執筆者Richard Webbは付け加える:「一方、WiMAXの長期的展望は新たな潜在的市場の多様化に依存するでしょう。新たに浮上したスマートグリッド部門においてビジネスチャンスは拡大しており、例えば、WiMAXのベンダー--WiMAX Forumは最近、スマート・グリッド・ワーキンググループを始め、我々はユーティリティー・プロバイダから更に多くの契約を確認しています--にとっては、WiFiバックホール・ソリューションとしてニッチな需要を見いだす事はもちろん、実り多い市場である事が判明しています」

2G、3G、4Gモバイル・インフラ市場のハイライト

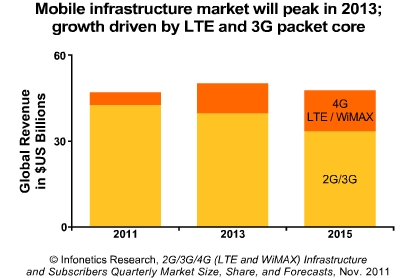

- 2011年第3四半期、LTE及びWiMAX装置を含む2G/3G/4Gインフラ市場全般において、全世界合計で108億ドル、2010年第3四半期比で8.6%上昇し、季節要因から4%低下した。

- 世界的なLTE装置の収益は2011年第2四半期から2011年第3四半期にかけて連続的に38%急上昇し、今やWiMAX装置市場の2倍以上に成長した。

- 2011年第3四半期において、4G市場(LTEとWiMAXの合計)は「1四半期あたり10億ドル収入」のハードルをクリアした。

- Alcatel-Lucentは2011年第3四半期に、LTE 市場における激しいシェア争いの結果、Ericssonとは1ポイント以下の僅差でナンバーワンの座についた。

- HuaweiはSamsungを抜き、2011年第3四半期におけるWiMAX市場占有率1位の収益を稼ぎ出した。

Infonetics' quarterly 2G/3G/4G (LTE and WiMAX) Infrastructure and Subscribers report provides worldwide and regional market size, vendor market share, analysis, and forecasts for LTE, WiMAX, and 2G/3G mobile network equipment and subscribers. The comprehensive report tracks more than 50 sub-segments of the market, from radio access network (RAN) macrocell, microcell, and picocell base transceiver stations (BTS) and mobile softswitching to packet core equipment, E-UTRAN macrocells and all flavors of WiMAX, and includes deployment trackers for WiMAX and LTE. Vendors tracked: Acme Packet, Airspan, Alcatel-Lucent, Alvarion, Apertio, Aperto, Aviat, Cisco, Datang Mobile, Ericsson, Fujitsu, GENBAND, HP, Huawei, Motorola, NEC, Nokia Siemens, Proxim, Redline, Samsung, Tellabs, UTStarcom, ZTE, and many others.

RELATED NEWS

- Mobile network optimization / self-organizing network (SON) market nearing $3B by 2015

- Telecom capex up 6% to $311B in 2011, rev. up 8% to $1.86T, driven by mobile broadband

- Mobile VoIP subscribers will near 410 million by 2015; VoLTE still a long way off

- LTE survey shows 3/4 of operators deploy HSPA+ before LTE

European Union sovereign-debt crisis having minimal impact on telecoms; LTE equipment up 38% in 3Q11

Campbell, CALIFORNIA, Dec. 1, 2011-Market research firm Infonetics Research today released excerpts from its third quarter 2011 (3Q11) 2G/3G/4G (LTE and WiMAX) Infrastructure and Subscribers report, which takes a comprehensive look at the mobile and wireless equipment markets, including vendor market share, forecasts, and LTE and WIMAX deployments.

ANALYST NOTE

"What many people seem to be overlooking in the midst of the European Union sovereign-debt crisis is that the EU's 'Big 5' telecom operators -- Deutsche Telekom, France Telecom, Telecom Italia, Telefonica, Vodafone -- are cash rich, each with more than ?10 billion in cash!" points out Stephane Teral, principal analyst for mobile infrastructure at Infonetics Research. "Yes, there are definitely challenges, and many telecom carriers, particularly in Europe and the Middle East, are going to have a tough time generating new revenue, but the fact remains that the telecom world is not falling apart. The fundamentals of the market are intact; service providers must continue upgrading their networks to manage relentlessly growing traffic. As a result, we maintain our view that this crisis continues to have minimal impact on telecoms overall."

Teral adds: "So, despite a sequentially down third quarter for the overall 2G, 3G, and 4G mobile infrastructure market, which any vendor will tell you was due to seasonality (the third quarter has been down in 4 of the last 5 years), the market is up nearly 9% from the year-ago quarter. Lighting the way is the LTE equipment segment, up 330% from a year ago. Now that Verizon's LTE spending has passed its peak, the 'LTE 2nd wave' has begun, led by AT&T and other operators around the world, along with the earlier-than-expected ramp up from Sprint. Combined, these activities are helping LTE take off even faster, prompting us to increase our LTE forecast."

Richard Webb, directing analyst for microwave and small cells at Infonetics Research and co-author of the report, adds: "Meanwhile, the long-term future of WiMAX will depend on diversification into new addressable markets. Opportunities have expanded into the emerging smart grid segment, for instance, which is proving fruitful for WiMAX vendors -- the WiMAX Forum has recently initiated its Smart Grid Working Group, and we are seeing more contracts from utility providers -- as well as finding a niche as a WiFi backhaul solution."

2G, 3G, 4G MOBILE INFRASTRUCTURE MARKET HIGHLIGHTS

- In 3Q11, the overall 2G, 3G, and 4G infrastructure market, including LTE and WiMAX equipment, totaled $10.8 billion worldwide, up 8.6% from 3Q10, and down 4% sequentially due to seasonality

- Global LTE equipment revenue jumped 38% sequentially in 3Q11 over 2Q11, and is now more than twice the size of the WiMAX equipment market

- In 3Q11, the 4G market (LTE and WiMAX combined) passed the $1-billion-per-quarter bar

- Alcatel-Lucent held on to its hotly contested number-one position in the LTE market in 3Q11, less than one market share point ahead of Ericsson

- Huawei beat Samsung for first place in WiMAX revenue market share in 3Q11