1012年1月19日ロンドン発――市場調査会社のInfonetics Researchは、先日、企業顧客に対して、フェムトセル、モバイルPBXの拡張製品、ユニファイドコミュニケーション (UC)、デュアルモードWiFi/携帯サービスなど、フェムトセルおよび固定―モバイルの融合サービス (FMC) を提供する計画について、通信事業各社の調査を実施した。

同社は調査結果を『Enterprise Femtocell and FMC Services: Global Service Provider Survey (仮訳: 企業向けフェムトセル&FMCサービス:世界のサービスプロバイダ調査)』として発行。フェムトセル・FMCサービスに向けての通信事業各社の戦略的ロードマップ――フェムトセルサービスをより洗練されたサービスに進化させるために、どのようなことを計画しているか、そして、FMCをどう企業向けサービスに統合できるか――を詳細分析・解説した。

アナリストノート

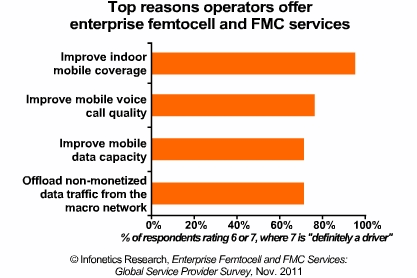

「2011年~2012年の同市場には、目覚しいほどの活性化が見られるが、企業向けフェムトセルは、まだあまりに若い市場分野です。これほど早い段階とあって、ほとんどの企業はまだ慎重に事を進めています。企業向けフェムトセル・ソリューションでネットワーク・カバレッジを上げたり (モバイル通信事業者にとっては、大事な企業顧客との関係が拗れかねない挑戦)、モバイル音声通話の品質向上、モバイル・データ容量を拡大したりといった動きが見られます。

改善が進み、容量やカバレッジに関する基本的ニーズが、いったん満たされた後には、より洗練された他のFMCサービスが控えています。」とInfonetics Research社でマイクロ波、モバイル・オフロード、モバイル・ブロードバンド装置を担当する主席アナリスト、リチャード・ウェブ (Richard Webb) 氏は述べる。

企業向けフェムトセル・FMC調査のハイライト

- Infonetics社の調査に協力した通信事業者の61%は、すでに企業に対して、フェムトセルやFMCの売り込みを行っており、29%は2012年内、10%は2013年内に、同サービスを開始する予定である (Infonetics社は、フェムトセル・FMCサービスを現在、提供しているか、今後、2013年末までに提供する予定の通信事業者のみに対して、聞き取り調査を行った。

- フェムトセルは、無線屋内カバレッジや容量を提供するための技術として、最初に登場しており、今後2013年までで、最も成長が見込まれる分野である。その後は、マイクロセル/ピコセルや分散アンテナシステム (DAS) の時代となるだろう。

- 通信事業者各社は、複数のソリューションを用意して、無線屋内カバレッジや容量の提供を行っているが、恐らくは、フェムトセルのコスト効率が、最も高いうえ、カバレッジと容量が両方とも改善できる。これは、他のFMC (DASなど) には実現できていないことだ。

- 回答を寄せた通信事業者のうち、デュアル・モード3G/WiFiフェムトセルの配備を進める会社は、2011年の5%から2013年の38%にまで上昇する。

- 企業向けフェムトセル・サービスの開発という点では、同技術の提供先を比較的小規模な企業に絞って売り込んでいる比較的小規模な競合モバイル通信事業者各社の方が、進んでいる。

For its Enterprise Femtocell and FMC Services: Global Service Provider Survey, Infonetics analysts interviewed 21 mobile, incumbent, competitive, and cable operators that offer enterprise femtocell and FMC services or will by 2013. The respondents are from Europe, Asia Pacific, North America, and the Middle East -- the key areas of femtocell activity to date -- and together represent 33% of worldwide telecom carrier revenue and 31% of capex. Operators were asked about current and future enterprise femtocell technologies used, types deployed, services supported, strategies, subscribers, and more.

(原文)

Operators turn to femtocells to improve enterprise coverage and capacity

London, UK, January 19, 2012-Technology market research firm Infonetics Research recently surveyed operators about their plans to provide enterprise customers with femtocell and fixed-mobile convergence (FMC) services, such as enterprise femtocells, mobile PBX extension, unified communications, and dual-mode WiFi/cellular services.

The results are published in Infonetics' Enterprise Femtocell and FMC Services: Global Service Provider Survey, which takes a deep dive into operators' strategic roadmap for femtocell and FMC services, how they plan to evolve femtocell services into more sophisticated offerings in the future, and how they can integrate FMC for enterprise users.

ANALYST NOTE

"Although there was a notable injection of impetus into the market in 2010 and 2011, the enterprise femtocell segment is still very young. At this early stage, most operators are proceeding cautiously, launching enterprise femtocell solutions to improve in-building network coverage (a challenge for mobile operators that can strain relations with high-value enterprise customers), mobile voice call quality, and mobile data capacity. Once the basic needs of capacity and coverage are improved, the opportunity to sell other, more sophisticated FMC services will follow," expects Richard Webb, directing analyst for microwave, mobile offload and mobile broadband devices at Infonetics Research.

ENTERPRISE FEMTOCELL AND FMC SURVEY HIGHLIGHTS

- 61% of the operators participating in Infonetics' survey already offer femtocell and FMC services to enterprises, 29% plan to offer the services in 2012, and 10% by 2013 (Infonetics interviewed only operators that currently offer femtocell and FMC services or plan to by 2013)

- Femtocells top the list of technologies used to deliver wireless indoor coverage and capacity and show the most growth between now and 2013, followed by microcells/picocells and distributed antenna systems (DAS)

- While operators use multiple solutions to provide wireless indoor coverage and capacity, femtocells are arguably the most cost effective, and improve capacity as well as coverage, which not all alternatives (such as DAS) do

- The percentage of respondent operators deploying dual-mode 3G/WiFi femtocells jumps from 5% in 2011 to 38% in 2013

- Smaller competitive mobile operators are more advanced in the development of their enterprise femtocell service offerings, using the technology to target smaller businesses