2013年6月7日米国マサチューセッツ州ボストン発―Infonetics Researchは、2013年の SDP Strategies and Vendor Leadership: Global Service Provider Survey からその概要をリリースした。ここではオペレータによるサービスデリバリープラットフォーム (SDP: Service Delivery Pltaform))採用戦略、採用を促進しているアプリケーション、SDP市場における主要ベンダーに対する評価を取り扱っている。

アナリストノート

「新サービスの市場導入にかかる時間が短くなりopex(営業経費)が減少するというSDP (サービスデリバリープラットフォーム投資の背景にある基本的なドライバーの多くはそれほど変化していないが、オペレータは紛れもなくSDPをネットワークから収益をもたらし、OTTプロバイダが自社利益にもたらす悪影響を管理するものとみている」と、Infonetics Researchでサービスイネーブルメントと加入者インテリジェンスを担当している上席アナリストShira Levineは述べている。

Levine は、「それでも、SDPを実施する費用はその採用に対する大きな障害となっており、オペレータは商用既製ソフトウェアなど、より製品化されたソリューションに目を向けている」とも述べている。

SDPサーベイのハイライト

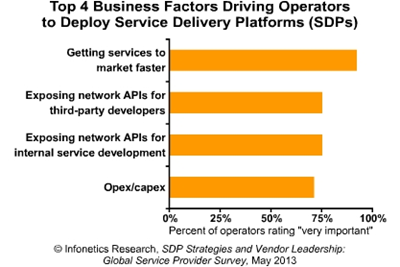

- 「サービスをいち早く市場に提供する」は、サービスデリバリープラットフォーム(SDP)投資に対する最も主要な要因であると調査対象企業は回答している。僅差で「サードパーティデベロッパーや社内開発チーム向けネットワークAPIを広める」が続く。

- 調査対象オペレータの46%は、自社SDPがごくわずかなカスタマイゼーションを伴う商用既製(COTS)ソフトウェアを主たるベースとしているか、今後そうなるだろうと回答している。

- 調査対象オペレータの半分は、自社のIT部門をSDP購入の意思決定に係る経理上の権限があると回答しており、33%はマーケティング部門であるとしている。

- SDPベンダーのトップ3について自由回答で質問したところ、プロバイダが挙げたのは Ericsson (第1位)、 HuaweiとOracle (第2位タイ)、IBM (第3位)であった。Huawei はInfonetics' 2012 SDP survey で第1位であった。

For its 22-page SDP strategies and vendor leadership survey, Infonetics interviewed purchase-decision makers at mobile and convergent operators in Europe, Asia Pacific, the Middle East and Africa, and North America that have SDPs in place or plan to by 2014. The report covers SDP deployment strategies, drivers, barriers, features, and vendors. SDP vendors examined: Accenture, Aepona, Alcatel-Lucent, Ericsson, Huawei, HP, IBM, Nokia Siemens Networks, Opencloud, Oracle.

(原文)

Operators look to monetize networks, stave off OTT threat via service delivery platforms

Boston, MASSACHUSETTS, June 6, 2013-Market research firm Infonetics Research released excerpts from its 2013 SDP Strategies and Vendor Leadership: Global Service Provider Survey, which explores operators' strategies for deploying service delivery platforms (SDPs), applications driving their deployments, and their views of the major vendors playing in the SDP market.

ANALYST NOTE

"Though many of the basic drivers behind SDP (service delivery platform) investments haven't changed - things like shortening time to market for new services and reducing opex - operators are definitely looking to SDPs to monetize their networks and manage the impact of over-the-top providers on the bottom line," notes Shira Levine, directing analyst for service enablement and subscriber intelligence at Infonetics Research.

Levine continues: "Still, the cost of implementing an SDP is a major barrier to deployment, and operators are turning to more productized solutions, including commercial off-the-shelf software."

SDP SURVEY HIGHLIGHTS

- Getting services to market faster is overwhelmingly the top business driver behind survey respondents' service delivery platform (SDP) investments, followed closely by exposing network APIs for 3rd-party developers and internal development teams

- 46% of operators surveyed say their SDPs are or will be based primarily on commercial off-the-shelf (COTS) software with only minor customization

- Half of respondent operators named their IT department as the group that holds the purse strings for SDP purchase decisions, and 33% named marketing

- When asked in an open-ended question who they consider to be the top 3 SDP vendors, service providers most often named Ericsson (#1), Huawei and Oracle (tied for #2), and IBM (#3); Huawei was #1 in Infonetics' 2012 SDP survey