2013年6月20日米国カリフォルニア州キャンベル発―Infonetics Researchは、2013年第1四半期版 (1Q13) 2G、3G、4Gモバイルインフラと加入者に関するレポートからの抜粋を公表した。レポートでは、2G、3G、LTE、およびWiMAXネットワーク機器と加入者について追跡調査している。

アナリストノート

Infonetics Researchでモバイルインフラと通信事業者経済を担当する主席アナリストStephane Teral氏は次のように述べる。「当社は、広範なLTEへの移行とそれが2G、3G、WiMAXに直接与える影響を目の当たりにしています。通常なら2G、3Gが強い市場、特に中国も、今回は救援の手を差し伸べませんでした。事実、中国とロシアは2013年の第1四半期中、LTEベンダーの選択に忙しくしていました。もはや、LTEなしの生活は地獄! なのです。」

Infonetics Researchでマイクロ波、通信事業者WiFiを担当するアナリストRichard Webb氏はこう付け加えた。「LTEは当社の長期的な2G/3G/4Gインフラ予測の重要項目です。2012年から2017年の5年間、16%のCAGRで成長するものと見ています。」

モバイルインフラ市場のハイライト

- 2013年第1四半期、世界の2G/3G/4Gモバイルインフラ市場は、LTEが北米と欧州で増加したにもかかわらず、前期比9%、前年同期比2%の減少で98億ドル規模だった。

- Infoneticsでは日本円に対する米ドルの上昇で収益の少なくとも5%が消えたと見ているものの、2013年第1四半期のLTEの収益は27億ドルで、前期比21%、前年同期比108%の増加だった。

- 2013年第1四半期、WiMAXは前期から42%減少し落ち込みが続いた。

- 2012年第4四半期の落ち込みの後、BRIC諸国 (ブラジル、ロシア、インド、中国) は2013年を牽引する主要なエンジンとなるべく体勢を整えており、その適例としては、ブラジルのモバイル事業者4社がLTEを発表し、2013年第1四半期の収益の中に加わったことが挙げられる。

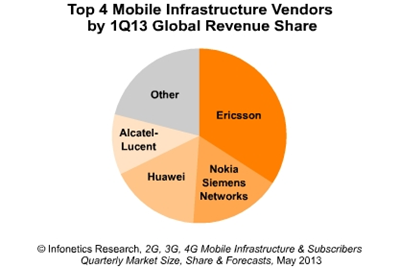

- Ericssonは市場収益シェアで業界第2位のNokia Siemens Networksの倍を占め、依然RANの王として君臨している。

- Infoneticsは、W-CDMAだけで前進しているGSMよりも3G RANの方が優勢であり続けると予想している。

- 世界のモバイル加入者数は、2017年までに70億人に達し、LTE加入者が全体のちょうど8%を占めるようになるとInfoneticsは予測している。

Infonetics' quarterly 2G, 3G, 4G (LTE) report provides worldwide and regional market size, vendor market share, analysis, deployment trackers, and forecasts through 2017 for 2G, 3G, 4G (LTE), and WiMAX mobile network equipment and subscribers. The report tracks more than 50 subsegments of the market, including radio access networks (RAN), base transceiver stations (BTSs), mobile softswitching, packet core equipment, and E-UTRAN macrocells. Vendors tracked: Airspan, Alcatel-Lucent, Alvarion, Cisco, Datang Mobile, Ericsson, Fujitsu, Genband, HP, Huawei, NEC, NewNet, Nokia Siemens Networks, Proxim, Redline Communications, Samsung, UTStarcom, ZTE, and others.

(原文)

LTE not enough to lift mobile infrastructure market in Q1

Campbell, CALIFORNIA, June 20, 2013-Market research firm Infonetics Research released excerpts from its 1st quarter 2013 (1Q13) 2G, 3G, 4G Mobile Infrastructure and Subscribers report, which tracks 2G, 3G, LTE, and WiMAX network equipment and subscribers.

ANALYST NOTE

"We are clearly seeing the broad shift to LTE and its direct effect on 2G, 3G, and WiMAX," notes Stephane Teral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research. "Typically strong 2G and 3G markets, China in particular, did not come to the rescue this time around. In fact, China and Russia had a busy 1Q13 selecting LTE vendors. Life without LTE would be hell!"

Richard Webb, directing analyst for microwave and carrier WiFi at Infonetics, adds: "LTE is the highlight of our long-term 2G/3G/4G infrastructure forecast, growing at a 16% CAGR over the 5 years from 2012 to 2017."

MOBILE INFRASTRUCTURE MARKET HIGHLIGHTS

- In 1Q13, the worldwide 2G/3G/4G mobile infrastructure market totaled $9.8 billion, down 9% sequentially, and down 2% year-over-year, despite another LTE ramp-up driven by North America and Europe

- LTE revenue was $2.7 billion in 1Q13, an increase of 21% quarter-over-quarter and 108% year-over-year, though Infonetics believes an appreciation of the U.S. dollar against the Japanese Yen erased at least 5% of revenue

- WiMAX continued its decline, dropping 42% in 1Q13 from the previous quarter

- After dragging down 4Q12, the BRIC countries (Brazil, Russia, India, China) are shaping up as a major engine for 2013; case in point: Brazil added to the 1Q13 revenue mix when its 4 mobile operators kicked off LTE rollouts

- Ericsson remains king of the RAN, with double the revenue market share of #2 Nokia Siemens Networks

- Infonetics expects 3G RAN to continue to be greater than GSM moving forward solely driven by W-CDMA

- Global mobile subscribers are forecast by Infonetics to reach 7 billion by 2017, with LTE subscribers making up just 8% of total subscribers