2013年12月6日米国マサチューセッツ州ボストン発―Infonetics Researchは多様な支払い方法、サービスタイプ、ネットワーク・アクセスを含む様々な面を統合処理する為に構築された課金ソフトウェアと、それに関連したコンサルティング、インテグレーション、マネージメント・サービスについて調査した、最新の統合課金ソフトウェア及びサービス リポートからの抜粋をリリースした。

アナリストノート

「迅速かつ効率的に新しいサービスと価格提供を行う事が可能になるように、事業者達が第1世代の課金システムをスワップアウトして拡縮可能で柔軟性のあるソリューションに交換するという動きが活発化したのも牽引要因の一つとなって、統合課金マーケットは健康な成長が継続しています。」Infonetics Researchのサービス・イネーブルメント及び加入者インテリジェンス担当監督アナリストShira Levineは報告する。

「我々は次の数年に渡って、LTEの導入が更にマーケットを加速すると予測しています。」続けてLevineは語る。「通信事業者は新しいサービスと、消費されるバンド幅をより密接に請求価格と結び付けた価格設定モデルによって、LTEのより大きな『パイプ』をフル活用することを望むでしょう。」

統合課金市場のハイライト

- 統合課金は全体としてはLTEの展開と手を携えていないが、その代わりにLTEは間接的な牽引役を務めている。

- モバイル・ネットワーク上において、米国のマシンツーマシン(M2M)通信取引は最終的に人間同士の取引を遥かに超える事が予想されており、Infonetics は大多数の通信事業者がビジネスにおけるこの新しい流れをサポートする為に-既存のシステムを延長するよりも-新しい課金処理スタックを実施するであろうとを予測している。

- 次の12~18ヶ月に渡って、契約者のプラン変更、手軽な搭載、モニター使用などを可能にするセルフケア機能を含んだ、サービスと出費に関してより良いコントロールをもたらすような統合課金ソリューションに対する更に大規模な強化があるだろう。

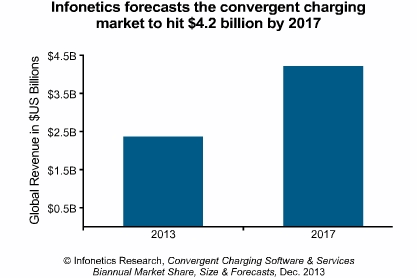

- Infoneticsは新興成長市場における認可の増加と開拓済市場におけるサービス出費からの成長によって、統合課金マーケットが2017年には42億ドル市場に達すると予測している。

- Infonetics' biannual convergent charging report provides worldwide and regional market size, market share, forecasts through 2017, analysis, and trends for convergent charging software and services, and includes a convergent charging product roadmap and strategic outlook. Vendors tracked: Alcatel-Lucent, Amdocs, Convergys, Comverse, CSG Systems, Ericsson, Hewlett-Packard, Huawei, NSN, Openet, Oracle, Orga Systems, Volubill, and others.

Convergent charging market lifting as operators replace first-gen systems and roll out LTE

Boston, MASSACHUSETTS, December 6, 2013-Market research firm Infonetics Research released excerpts from its latest Convergent Charging Software and Services report, which tracks charging software built to handle multiple dimensions of convergence, including convergence across payment methods, service types, and access networks, along with related consulting, integration, and managed services.

ANALYST NOTE

"Healthy growth in the convergent charging market continues, driven in part by a wave of replacement activity as operators swap out their first-generation charging systems for more scalable and flexible solutions that allow them to get new services and offers to the market quickly and efficiently," reports Shira Levine, directing analyst for service enablement and subscriber intelligence at Infonetics Research.

"We expect LTE rollouts to further accelerate the market over the next few years," continues Levine. "Operators will want to capitalize on LTE's bigger 'pipe' via new services and pricing models that better tie the bandwidth consumed to the price being charged."

CONVERGENT CHARGING MARKET HIGHLIGHTS

- Convergent charging spending is generally not occurring hand-in-hand with LTE deployments; instead, LTE is acting as an indirect driver

- M2M transactions are expected to eventually far exceed human transactions on the mobile network, and Infonetics anticipates that most operators will implement new charging stacks-rather than extending existing systems-to support this new line of business

- Over the next 12-18 months, there will be a greater emphasis on convergent charging solutions that include self-care capabilities, enabling subscribers to change plans, add bolt-ons, and monitor usage, gaining more control over their services and spending

- Infonetics forecasts the convergent charging market to reach $4.2 billion in 2017, with growth coming from an increase in licenses in emerging markets and services spending in developed markets