アナリストノート

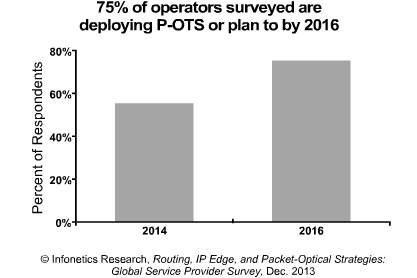

「サービスプロバイダとベンダーは光伝送をより一層活用する方法を検討してきましたが、それにはパケット・トラフィックの伝送媒体として不可欠なパケット機能の役割を果たす、ルータに代わる選択肢としての活用も含まれます。」Infonetics Researchの共同創設者兼キャリア・ネットワーク担当主任アナリストMichael Howardは解説する。「我々が聞き取り調査を行った事業者の75%が、今、もしくは2016年までにP-OTS(パケット-光統合伝送システム)の使用を計画しており、弊社による最新のルーティング戦略調査はキャリア・ネットワークの分野で大規模な変化が進行中である事を裏付けています。」

アナリストノート

「サービスプロバイダとベンダーは光伝送をより一層活用する方法を検討してきましたが、それにはパケット・トラフィックの伝送媒体として不可欠なパケット機能の役割を果たす、ルータに代わる選択肢としての活用も含まれます。」Infonetics Researchの共同創設者兼キャリア・ネットワーク担当主任アナリストMichael Howardは解説する。「我々が聞き取り調査を行った事業者の75%が、今、もしくは2016年までにP-OTS(パケット-光統合伝送システム)の使用を計画しており、弊社による最新のルーティング戦略調査はキャリア・ネットワークの分野で大規模な変化が進行中である事を裏付けています。」Howardは付け加える。「広域通信事業者も同様に100GEに大いに興味を持っています。我々は彼等が異なるアプリケーション- データセンター接続、アグリゲーション、コア、その他 -の為に100GEをいくらで、そしていつまでに購入するつもりがあるのか尋ねました。一部の事業者は現在の必要に応じて、既に100GEに対して10GEの15倍の価格を支払っています。そして我々は、一部の事業者は、自社ネットワークの特定の部分の為に100GEに更に多くを進んで支払うであろう事に気付きました。例えば彼等の1/3以上が、光ファイバの処理能力が低いルータに対して割増金を支払う事を厭いません。とはいえ未だ大部分の広域通信事業者は、100GEの価格設定が10GEの10倍かそれ以下になるまで待つと思われるので、製造業者は100GEの価格を下げる為に開発努力を続けるべきでしょう。」 ルーティング戦略調査のハイライト

- 通信事業者は、彼等が購入した全ての10/40/100GEルータ・ポートのうちの100GEポートの占める割合が、2013年の5%から、2015年には30%まで増えると予測する。

- ビデオ、モバイル性、クラウド・サービスのプレッシャーから、プロバイダは中央集中型の「スーパーPOP」から、メトロ・エリア内の5から10のスーパーCOで構成された多数の大きな次世代セントラル・オフィス(NG-COs)へと多機能を分散する事によって、自社メトロ・ネットワークの再構築を進めている。

- これらの機能分散にはブロードバンドのリモートアクセス・サーバ(BRAS)、コンテンツ配信網(CDNs)、キャッシングも含まれ、コロケーションとクラウド・サービスの為に「ミニ・データセンター」にサーバとストレージが実装され、そしてソフトウェアによって定義されたネットワーク(SDN)がサービスを繋ぐ事によって、ネットワーク機能仮想化(NFV)を使用した住宅や企業の顧客に対する(セキュリティのような)サービスを提供する能力もある。

- Infonetics' December 2013 25-page routing startegies survey, is based on interviews with router and switch purchase-decision makers at incumbent, independent wireless, competitive, and cable operators from around the world. The report provides insights into 10/40/100GE port purchases, P-OTS deployment plans, multilayer data/transport control plane demand, CDN deployment drivers, and fixed-mobile network convergence strategies. Respondents control 36% of 2012 worldwide service provider capex and 32% of revenue.

Major network changes underway, this time to 100GE and packet-optical Campbell, CALIFORNIA, December 27, 2013-Market research firm Infonetics Research released excerpts from its 2013 Routing, IP Edge, and Packet-Optical Strategies: Global Service Provider Survey, which focuses on 100 Gigabit Ethernet (100GE) adoption and pricing expectations, usage of packet-optical transport systems (P-OTS), and the architectural changes occurring to metro networks in next-generation central offices (NG-COs). ANALYST NOTE "Service providers and vendors have been talking about how to use more optical transport with essential packet functionality to serve as the transport vehicle for packet traffic as an alternative to routers," explains Michael Howard, Infonetics Research's co-founder and principal analyst for carrier networks. "Our latest routing strategies study confirms that major changes are underway in carrier networks, with 75% of the operators we talked to using P-OTS (packet-optical transport systems) now or planning to by 2016."

Howard adds: "Carriers are very interested in 100GE as well. We asked at what price they would buy 100GE for different applications - data center connections, aggregation, core, etc. - and by when. Some operators are already paying 15 times the price of 10GE for 100GE because they need it now, and we found that some operators are willing to pay more for 100GE for specific parts of their networks; for example, over a third are willing to pay a premium for routes with low fiber availability. Still, most carriers will wait until 100GE pricing comes down to 10 times 10GE or lower, so it behooves manufacturers to continue developments that lower the price of 100GE." ROUTING STRATEGIES SURVEY HIGHLIGHTS

- Operators expect 100GE ports to grow from 5% of all their 10/40/100GE router port purchases in 2013 to 30% in 2015

- Due to the pressures of video, mobility, and cloud services, providers are re-architecting their metro networks by distributing a number of functions from a single central "super POP" to a number of large next-generation central offices (NG-COs) made up of 5 to 10 super COs in a metro area

- These distributed functions include broadband remote access servers (BRAS), content delivery networks (CDNs) and caching, deploying servers and storage in "mini data centers" for colocation and cloud services, and the ability to offer services (such as security) to residential and business customers using network functions virtualization (NFV) with software-defined network (SDN) service chaining