アナリストノート

Infonetics Researchでキャリア伝送ネットワーク担当の主席アナリストを務めるAndrew Schmitt氏は次のように言う。「100Gおよび100G超のコヒーレント装置・部品ベンダーにとっての主戦場は、大勢を占める主要アプリケーションの勝者が決定したことから、メトロネットワークへと移行しました。」

アナリストノート

Infonetics Researchでキャリア伝送ネットワーク担当の主席アナリストを務めるAndrew Schmitt氏は次のように言う。「100Gおよび100G超のコヒーレント装置・部品ベンダーにとっての主戦場は、大勢を占める主要アプリケーションの勝者が決定したことから、メトロネットワークへと移行しました。」Schmitt氏はこう続ける。「コヒーレント技術には非常に異なる2つの市場があります。1つの市場は現在、長距離コヒーレントを展開しており、これから数年のうちにメトロネットワークに移行していくでしょう。しかし、一方で、現在既にメトロネットワークでのコヒーレント技術の展開に全面的に取り組んでいる別のタイプの取引先があります。これら2つの市場は、製品の専門化におけるサプライチェーンや、フレックス コヒーレント技術への関心が一部の取引先で相対的に低い状況に対して重大な影響を与えています。」 100G+およびROADM調査のハイライト

- 回答事業者は、コアネットワークに対するコヒーレント 地域内メトロネットワークおよびアクセス アプリケーションの価格設定について妥当な予測をしている。

- メトロ100G向けアプリケーションに関して言えば、調査参加者は今後12ヶ月間にわたって、データセンター間の相互接続が明確なキラーアプリケーションになると見ている。

- 過去数年のInfonetics調査と比較すると、回答者は100GE伝送の採用がさらに進むとも予測している。

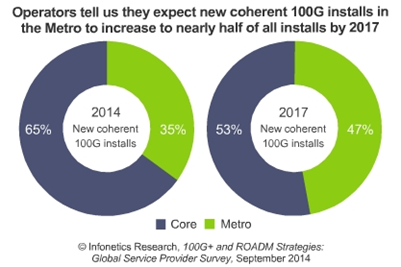

- 調査対象者は、2017年に100G WDMが、導入されるすべてのメトロ波長のほぼ40%とコアネットワークの75%を占めるようになると予測している。

- プラグイン可能なCFPおよびCFP2トランシーバー技術は、今年になって昨年よりもメトロネットワークにとってより重要な技術だと回答者たちに認識されている。

Battleground for 100G+ coherent gear and components shifting to the metro, shows Infonetics survey Boston, MASSACHUSETTS, October 2, 2014-Market research firm Infonetics Research released excerpts from its 2014 100G+ and ROADM Strategies: Global Service Provider Survey, which details the plans of operators transitioning optical transmission and switching equipment to higher-speed 100G+ wavelengths. ANALYST NOTE "The big battleground for vendors of 100G-and-beyond coherent equipment and components has shifted to the metro as winners for long reach core applications have been decided," says Andrew Schmitt, principal analyst for carrier transport networking at Infonetics Research.

"There are two very distinct markets for coherent technology. One market is deploying long haul coherent today and will transition to metro in the coming years. But there is another, separate customer type that is already fully committed to deploying coherent technology in the metro today," Schmitt adds. "These two markets have major implications for the supply chain regarding product specialization and the relative lack of interest in flex coherent technology by some customers." 100G+ AND ROADM SURVEY HIGHLIGHTS

- Respondent operators have reasonable expectations for pricing for coherent metro-regional and access applications versus the core

- When it comes to end-use applications for metro 100G, study participants view data center interconnect as the clear killer app for the next 12 months

- Respondents also expect a greater uptake of 100GE transport when compared to previous years' Infonetics surveys

- Those surveyed expect 100G WDM to account for almost 40% of all metro wavelength deployments and 75% of the core network in 2017

- Pluggable CFP and CFP2 technology is perceived by respondents as a more important technology for the metro this year than it was last year