マサチューセッツ州ボストン、2011年6月29日—マーケットリサーチ会社であるInfonetics Researchは、IMS Services Strategies, Product Features, and Vendor Leadership: Global Service Provider Survey,からのサマリーを発表しました。ネットワーク内でIPマルチメディア(音声、ビデオ、データ)サブシステムの核となる機器を使用するキャリアが、IMS市場における彼らのニーズや評価およびトレンドについてインタビューを行いました。このレポートはその抜粋です。

アナリストノート

Infonetics Research社のVoIPおよびIMS担当ダイレクティングアナリストDiane Myersは、「当社の2011年度の通信事業者向けサーベイ結果から、固定電話のVoIPはIMSで展開しているサービスの中でも引き続き最も重要な位置を占めていることが示されたが、その一方で、IMSがモバイル分野にシフトする傾向にも注目が集まった。これは、2013年までのIMSにおけるモバイルサービス関連サービスの計画数の増大から明らかである。つまり、2013年までに、モバイル専門サービス、たとえばモバイルメッセージ、VoLTE(Voice Over LTE)、RCS(リッチコミュニケーションサービス)、および/または3G対応VoIPなどの所有率が現在の35%から上昇し、回答者の78%にのぼることになる。」と述べている。

IMS調査のハイライト

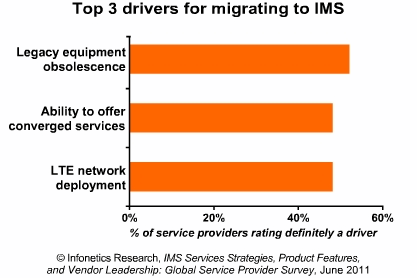

- IMSの展開を推進する2つの主要な要素は、集中的なサービスとLTE(ロングタームエボリューション)ネットワークの展開を提供する能力である。

- 2011年と2010年版のInfoneticsの調査のいずれについても、いずれかの要素を「明確な障壁」と位置づけた回答者が少なかったことから、IMSの展開にはこれ以上大きな障壁は残っていないと思われるが、既存の後端システムとの統合がリストの上位を占めている。

- InfoneticsのIMS調査に参加しているサービスプロバイダの少なくとも半数が、今後2年間でRCS、ビデオテレフォニー、ビデオ共有サービスに着手する予定である。

- インストール済み、および評価中の製品については、Nokia Siemens NetworksがCSCFおよびHSS業者のトップである。

- IMSインフラ業者の上位3社のうちトップはどこかという問いに対しては、EricssonとAlcatel-Lucentの名前を挙げるサービスプロバイダが最も多かった。

- HuaweiはEricsson、Alcatel-Lucent、およびNokia Siemens Networksに対して最大の競合・脅威として受け止められている。これは、キャリアの回答者が、サービスプロバイダの顧客獲得数に加え、価格と価値などのカテゴリーではHuaweiをトップと見なしているからである。

Infoneticsの2011年6月IMS survey(ページ数35)は、ネットワーク内でIMSの主要機器を使用する23社のサービスプロバイダにおける、知識豊富な購買決定権のあるメーカーとのインタビューを基にしている。合算でこのインタビューを受けたキャリアは世界中の通信事業の売上の30%、通信事業のCapex(資本支出)の29%を占める。また、これはEMEA(欧州、中東、アフリカ)、北米、太平洋地域の現役事業者(57%)、モバイル事業者(15%)およびケーブル事業者(9%)の混合である。

このレポートには、分析と質問へのキャリアからの回答が含まれている。質問は、IMSへの移行にあたる推進力と障壁、CSCF(コールセッション制御機能)およびHSS(自宅加入サーバー)の計画と重要な機能、IMSを基にした小売サービスの計画(企業がホストするIPボイス、SIPトランキング、クラス5代替ボイス、3G対応VoIP、IPTVなど)に関するものである。また、業者がサービスプロバイダを格付けするスコアカードも含まれる。格付け対象となるのは、IMSインフラメーカー8社(Acme Packet、Alcatel-Lucent、BroadSoft、Ericsson、GENBAND、Huawei、Nokia Siemens Networks、ZTE)であり、格付け基準は8つ(技術、製品、システム統合能力、価格対性能比、価格、財政面の安定性、サービスとサポート、ソリューション成熟度)である。また、業者のリーダーシップに関する自由回答式の質問への回答もある。

(原文)

IMS survey on services, equipment and vendors shows growing momentum for mobile services

Boston, MASSACHUSETTS, June 29, 2011—Market research firm Infonetics Research today released excerpts from its IMS Services Strategies, Product Features, and Vendor Leadership: Global Service Provider Survey, for which carriers with IP Multimedia (voice, video, data) Subsystem core equipment in their networks were interviewed to assess their needs and to analyze trends in the IMS market.

ANALYST NOTE

“Our 2011 survey results show that fixed-line VoIP continues to be the primary service deployed over IMS; however, there also is a notable continuing shift toward IMS in the mobile world, evidenced by the rising number of mobile services planned over IMS by 2013: 78% of our respondents will have a mobile-specific service such as mobile messaging, VoLTE (voice over LTE), RCS (Rich Communication Service), and/or VoIP over 3G by 2013, up from 35% today,” notes Diane Myers, directing analyst for VoIP and IMS at Infonetics Research.

IMS SURVEY HIGHLIGHTS

- 2 key factors driving IMS deployments are the ability to offer converged services and LTE (Long Term Evolution) network deployment

- While there appear to be no big barriers left to IMS deployment, indicated by the low numbers of respondents rating any factors “definitely a barrier” in either the 2011 or 2010 editions of Infonetics’ survey, integration with existing back-end systems tops the list

- At least half of the service providers participating in Infonetics’ IMS survey plan to launch RCS, video telephony, and video sharing services over the next 2 years

- Nokia Siemens Networks is the leading CSCF and HSS vendor in terms of products installed and under evaluation

- When asked who they consider to be among the top 3 IMS infrastructure vendors, service providers named Ericsson and Alcatel-Lucent the most

- Huawei poses a credible threat to Ericsson, Alcatel-Lucent, and Nokia Siemens Networks, as carrier respondents consider Huawei a leader in categories such as pricing and value, in addition to gaining service provider customers

Infonetics’ June 2011 35-page IMS survey is based on interviews with knowledgeable purchase-decision makers at 23 service providers with IMS core equipment in their networks. Together, the carriers represent a significant 30% of worldwide telecom revenue and 29% of telecom capex and are a mix of incumbents (57%), mobile operators (22%), competitive operators (13%), and cable operators (9%) from EMEA (Europe, Middle East, Africa), North America, and Asia Pacific.

The report includes analysis and carrier responses to questions about drivers and barriers for migrating to IMS, plans and important features for CSCF (Call Session Control Function) and HSS (Home Subscriber Servers), and plans for IMS-based retail services (business-hosted IP voice, SIP trunking, Class 5 replacement voice, VoIP over 3G, IPTV, etc.). The report includes a vendor scorecard with service provider ratings of 8 IMS infrastructure manufacturers (Acme Packet, Alcatel-Lucent, BroadSoft, Ericsson, GENBAND, Huawei, Nokia Siemens Networks, ZTE) on 8 criteria (technology, product roadmap, system integration capability, price-to-performance ratio, pricing, financial stability, service and support, and solution maturity), as well as responses to open-ended questions about vendor leadership.