2011年12月13日 Campbell, CALIFORNIA - 市場調査会社Infonetics Researchは本日、2011年第3四半期 (3Q11) の PON、FTTH、DSL統合機器と加入者数 (PON, FTTH, and DSL Aggregation Equipment and Subscribers) の市場占有率と予測レポートからの抜粋を公開した。このレポートでは固定ブロードバンドアクセス機器と加入者数を追跡調査している。

アナリストノート

Infonetics Researchのブロードバンドアクセスとビデオの主任アナリスト、Jeff Heynen氏は次のように予想している。「固定ブロードバンドアグリゲーション機器市場にとって、2011年がピークになると見込んでいる。中南米の DSLの成長、EMEA (ヨーロッパ、中東、アフリカ) 地域のVDSLとGPONの成長に加え、中国のPONへの支出急増が重なり、今年の支出額は非常に増えたが、ピークがあれば谷もある。つまり、今年のブロードバンドアグリゲーション機器市場では、79億ドルというこれまでの最高の支出が見込まれているが、2015年までには50億ドルまで落ち込むだろう。今年以降は中国と北米で支出が鈍り、通信事業者の重点はDSLからファイバーに移行するだろう。アクセス技術としてDSLが消えてしまうことはないが、世界の大手通信事業者の間では銅線を除去するという究極の目標のもと、ファイバーを過剰に構築する (Verisonなどが行なっている) 動きが続くだろう。」

PON、FTTH、DSL統合機器の市場ハイライト

- ヨーロッパ、中東、アフリカ(EMEA) 地域で2桁減少したことにより、世界のブロードバンドアグリゲーション (DSL、 PON および FTTH) 機器への支出は引き続き3%の減少を示し、2011年第3四半期には20億ドルとなった。

- ブロードバンドアグリゲーション機器への支出が増加したのはアジア太平洋地域のみで、引き続き3%増加した。

- 2010年第3四半期と2011年第3四半期の前年同期比では、世界の固定ブロードバンドアグリゲーション機器の収益は、15%の堅調な成長を示している。

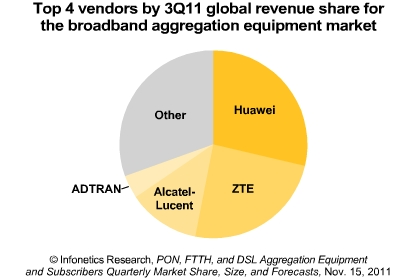

- Huawei とZTEはブロードバンドアグリゲーション機器の総収益でリードを保っているが、Huaweiの収益は減少し、ZTEは増加したことにより、双方の差は大幅に縮まった。

- 2011年第3四半期ではAlcatel-Lucentが市場の3位を確実に維持している。一方ではADTRANは北米のDSLの出荷が好調で4位につけた。

- 14%の増加だった前四半期の後、主要プロジェクトの減速といつもの第3四半期の軟調さのため、2011年第3四半期の世界のDSL機器への支出は9%減少した。

- NTTとKDDIが加入者をFTTB+VDSLからFTTHに変え、IPTVとブロードバンドビデオサービスを提供するためにFTTHインフラへの支出を増やしており、日本においてはEPONの光回線終端装置 (OLT) の収益は引き続き、2011年第3四半期に16%増加した。

Infonetics' quarterly PON, FTTH, and DSL Aggregation report provides worldwide and regional market size, market share, analysis, and forecasts through 2015. Revenue and ports are tracked for the following equipment: DSL aggregation (MSAPs, next gen DLCs, ATM and IP DSLAMs), BPON, 1.25G/2.5G EPON, 2.5G GPON, 10G EPON, 10G GPON, and Ethernet FTTH (CPE and service provider equipment). The report also tracks DSL subscribers by type (ADSL/ADSL2+, VDSL/VDSL2, G.SHDSL). Companies tracked: ADTRAN, Alcatel-Lucent, Allied Telesis, Calix, Ciena, Corecess, Dasan, ECI, Enablence, Ericsson, Fujitsu, Huawei, Iskratel, Millinet, Motorola, NEC, Nokia Siemens, Samsung, Sumitomo, Tellabs, UTStarcom, Zhone, ZTE, ZyXEL, and others.

RELATED BROADBAND RESEARCH

- Cable broadband equipment market up 14% from year-ago quarter; Cisco gains

- Telecom capex up 6% to $311B in 2011, revenue up 8% to $1.86T, driven by mobile broadband

- Operators looking at next gen FTTH technologies will wait for prices to drop

- GPON equipment investment in Europe, India and Middle East far outpaces subscribers

- Home networking device sales up in a normally-down first quarter

- High speed network port market to hit $52 billion in 2015 (1G, 10G, 40G, 100G)

- Residential gateway survey shows strong support for IPTV; Comtrend, Cisco top vendor list

Fixed broadband access equipment market set to peak in 2011

Campbell, CALIFORNIA, December 13, 2011-Market research firm Infonetics Research today released excerpts from its third quarter (3Q11) PON, FTTH, and DSL Aggregation Equipment and Subscribers market share and forecast report, which tracks fixed broadband access equipment and subscribers.

ANALYST NOTE

"We expect that 2011 is going to be the peak for the fixed broadband aggregation equipment market. The PON spending boom in China, coupled with DSL growth in Central and Latin America and VDSL and GPON growth in the EMEA region created a perfect storm of spending this year, but with peaks come valleys: by 2015, the broadband aggregation market will decline to $5.0 billion, from what we expect to be its high of $7.9 billion this year. Spending in China and North America will slow after this year, and the focus of operators will shift from DSL to fiber. DSL as an access technology will never disappear, but overbuilding with fiber (as Verizon and others have done) with the ultimate goal of removing copper will continue to grow among the world's largest operators," expects Jeff Heynen, directing analyst for broadband access and video at Infonetics Research.

PON, FTTH, AND DSL AGGREGATION MARKET HIGHLIGHTS

- Global spending on broadband aggregation (DSL, PON and FTTH) equipment declined 3% sequentially in 3Q11 to $2.0 billion, led by a double-digit drop in Europe, the Middle East, and Africa (EMEA)

- Asia Pacific is the only region to post an increase in broadband aggregation equipment spending, up 3% sequentially

- Year-over-year, from 3Q10 to 3Q11, global fixed broadband aggregation revenue is up a healthy 15%

- Huawei and ZTE continue their lead in overall broadband aggregation equipment revenue, though Huawei's revenue dropped while ZTE's increased, significantly narrowing the gap between the two

- Alcatel-Lucent maintains its solid 3rd place lead in the market in 3Q11, while ADTRAN -- thanks to its strong quarter shipping DSL in North America, moved into 4th position

- After a 14% increase last quarter, global spending on DSL equipment declined 9% in 3Q11, reflecting a slowdown in some major projects plus traditional third quarter softness

- EPON optical line terminal (OLT) revenue in Japan grew 16% sequentially in 3Q11, as NTT and KDDI increased their FTTH infrastructure spending to convert FTTB+VDSL subscribers to FTTH and deliver IPTV and broadband video services