キャンベル、カリフォルニア州、2012年2月23日-市場調査会社 Infonetics Research は本日、2011年第4四半期(4Q11)のサービス事業者ルーターおよびスィッチ (Service Provider Routers and Switches)ベンダー市場シェアレポートの概要を発表した。ここでは、IPエッジルーター、IPコアルーター、キャリアイーサネットスィッチ(CES)市場セグメントおよびこれらの市場の製造業を対象としている。

「2011年、キャリアルーターおよびスィッチの市場規模は2010年から8%増加して過去最高の145億ドルとなり、同市場はモバイルRAN インフラ市場に次いで2番目に大きい電気通信市場セグメントとなった。」と、Infonetics Researchの共同設立者でキャリアネットワークの主席アナリストであるMichael Howardはコメントしている。

Howardの追加コメント。「逆説的ではあるが、2011年の実績は市場の全体的な成長率の点で鈍化の兆しがみられる。」「その理由は、2桁成長が続いている最大市場のアジアと最小市場の中南米がキャリアルーターおよびスィッチ市場の頼みの綱となっているにもかかわらず、北米とEMEAが低迷しているからである。それでも、固定ブロードバンドのトラフィック増加と3GやLTEネットワーク上のモバイルブロードバンドトラフィックの爆発的増加に対応するために、多くのサービス提供事業者がモバイルバックホールを含めてアクセス、アグレゲーション、コアネットワークをアップグレードしているように、基礎的な市場の成長ドライバーは市場全体を牽引するだろう。」

サービス提供事業者のルーターおよびスィッチ市場のハイライト

- IPエッジルーター、IPコアルーター、キャリアイーサネットスィッチ(CES)を含むグローバルなサービス提供事業者のルーターおよびスィッチの市場規模は2011年最終四半期に11%増加し39億ドルとなった。

- 4Q11のIPエッジセグメント(IPエッジルーターとCESの合計)は12%増、年間ベースでは8%増。

- Cisco は健全なマージンを確保してIPエッジセグメント市場を引き続きリードしており、2011年にはグローバルな市場の約3分の1を占有するとみられる。一方で主要競合事業者(Alcatel-Lucent、 Huawei、 Juniper、 ZTE)は全て2011年にシェアを増加させた。

- Alcatel-Lucent は堅調な業績により4Q11にグローバルなルーター売上で業界2番手の地位を獲得した。同社は中核となるルーター製品がないにもかかわらず2011年のEMEAルーター売上でも2番手の地位を維持した。

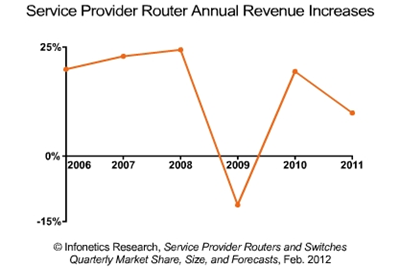

- キャリアルーターセグメントにおける最近のトレンドは、ルーターおよびスィッチ市場の全体的な動向を表している。つまり9.9%という相対的に低い成長がみられた景気後退のピーク2009年を例外として、2011年まで毎年ルーターの売上は2桁成長を示した。

- 4Q11の四半期ベースおよび2011年通年でみると、北米地域は、米国で経済成長の明るい兆しが多くみられたにもかかわらず、キャリアルーターとスィッチへの投資で唯一減少した地域である。

- 一方でEMEA地域は、低迷した1年であり、かつユーロ・ギリシャ・政府債務危機があったにもかかわらず、ルーターおよびスィッチへの投資で季節要因的な支出増がみられたため21%増となった。

- 南米およびメキシコではネットワークのアップグレードプロジェクトが進行しており、中南米地域における事業者ルーターおよびスィッチの関係事業者にとって好ましい1年となった(2011年に22%の売上増)。また、中国と日本はアジア市場を下支えした。

Infonetics' quarterly Service Provider Routers and Switches report tracks Alaxala, Alcatel-Lucent, Brocade, Ciena, Cisco, Ericsson, Extreme, Force10, Fujitsu, Hitachi Cable, Huawei, Juniper, NEC, Nokia Siemens, Orckit-Corrigent, Tellabs, ZTE, and others. The report provides worldwide and regional market share, market size, and analysis for IP edge routers, IP core routers, and CES. The report tracks the IP edge by application, including multiservice edge (MSE), broadband remote access server (BRAS), Ethernet access transport (EAT), and Ethernet service edge (MSE).

(原文)

Record year for carrier router and switch market in 2011, despite weakness in N. America

Campbell, CALIFORNIA, February 23, 2012-Market research firm Infonetics Research today released excerpts from its fourth quarter 2011 (4Q11) Service Provider Routers and Switches vendor market share report, which analyzes the IP edge router, IP core router, and carrier Ethernet switch (CES) market segments and the manufacturers within them.

"The carrier router and switch market hit a record-high $14.5 billion in 2011, up 8% over 2010, making it the second largest telecom market segment after mobile RAN infrastructure," notes Michael Howard, Infonetics Research's co-founder and principal analyst for carrier networks.

"Yet paradoxically, 2011 results show signs of a slowdown in the market's overall growth rate," Howard continues. "Why? Because despite continued double-digit percent annual growth in the largest market, Asia, and the smallest market, Latin America, the two mainstays of carrier routers and switches, North America and EMEA, are slowing. Still, the fundamental market drivers will pace the overall market forward, with growing fixed broadband traffic and exploding mobile broadband traffic on 3G and LTE networks pushing many service providers to upgrade their access, aggregation, and core networks, including mobile backhaul."

SERVICE PROVIDER ROUTER AND SWITCH MARKET HIGHLIGHTS

- The global service provider router and switch market, which includes IP edge routers, IP core routers, and carrier Ethernet switches (CES), grew 11% sequentially to $3.9 billion in the final quarter of 2011

- In 4Q11, the IP edge segment (the sum of IP edge routers and CES), jumped 12% sequentially and is up 8% for the year

- Cisco continues to lead the IP Edge segment by a healthy margin, commanding about a third of the global market in 2011, while its top competitors -- Alcatel-Lucent, Huawei, Juniper, ZTE -- all gained market share in 2011

- Alcatel-Lucent's strong performance propelled it into the #2 spot for global router revenue in 4Q11, and it retained #2 position for 2011 EMEA router revenue, despite not having a core router product

- Recent trends in the carrier router segment are indicative of the overall router and switch market: with the exception of 2009 during the height of the recession, router sales grew by double-digit percents each year until 2011, when they increased a relatively lower 9.9%

- North America is the only world region to post a decline in carrier router and switch spending both quarter-over-quarter in 4Q11 as well as for the full year 2011, despite the many economic growth signals in the US

- Meanwhile, EMEA had a seasonally typical budget flush, with a 21% pop in router and switch spending, despite a poorer year and the ongoing euro/Greece/debt/etc. crisis

- Ongoing network upgrade projects in South America and Mexico led to a banner year for service provider router and switch vendors in Latin America (revenue up 22% in 2011), and China and Japan propped up Asia