2012年12月20日、カリフォルニア州キャンベル-市場調査会社のInfonetics Researchは、Service Provider Capex, Revenue, and Capex by Equipment Typeレポートから抜粋を発表した。このレポートでは、通信事業者の収入と設備投資(CAPEX)について、通信事業者の形態、地域、機器の種類に分類して追跡調査すると共に、通信事業者の投資傾向に関する分析を提供している。

アナリストノート

「3四半期分のデータが手元に届き、主要な地域における通信事業者の投資計画を精査してみました。その結果によると、通信サービス事業者のCAPEXは、アジアと北米に支えられて今年は全体で4%近くまで上昇する見込みで、2013年は全地域で明るい結果となることが予想されます」

このように報告するのは、Infonetics Research でモバイルインフラ及びキャリア経済を担当する主席アナリストのStephane Teral。

「AT&TとDeutsche Telekomが出した投資計画と、世界各地に存在する大小様々の通信事業者による計画を合わせれば、2013年と2014年は、CAPEXがプラス成長になると確信を持って言うことができます。これはベンダーにとって朗報です。Deutsche Telekomが今月発表した300億ユーロ規模の3ヵ年投資計画は、EMEA地域に再び投資を呼び込むきっかけになるでしょう。サービスプロバイダは現在、自社ネットワークに投資せざるを得ない状況です。中にはCAPEXを長期間抑えすぎたために、ネットワークの稼働停止に見舞われ、爆発的に増加するトラフィックを処理できていない企業もあります。通信サービスは、特にモバイルブロードバンドなどにおいて、世界中で非常に大きな需要を集めています」

CAPEXレポートのハイライト

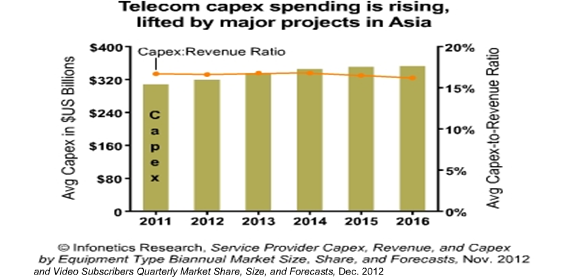

- 通信事業者のCAPEXは2012年に増加したが、その主な原動力となっているのは動画や無線へのインフラ投資である。

- サービスプロバイダの収入は、2012年に全世界で1.9兆米ドルに達し、2011年比で4%増となる見込みである。

- 既存の通信事業者による今年のCAPEXは、横ばいか若干低下となる。一方、独立系無線通信事業者、競合通信事業者、ケーブル通信事業者はそれぞれCAPEXを伸ばしており、中でも独立系無線通信事業者が今年、CAPEXを12%伸ばし牽引役となっている。

- 今年は、光及びTDMの音声機器を除き、全種類の通信機器において投資が増加すると見られる。

- 2015年にかけて投資対象となる主な分野は、ファイバー型の固定線ブロードバンド、2Gのモバイルネットワークの性能拡大、2Gから3Gへの移行、LTE事業への移行である。

- アジア太平洋地域は、サービスプロバイダによる収入で2016年には世界の約1/3を占めると見られる。収入と契約者数で世界最大のモバイル通信事業者であるChina Mobileがその推進力となる。

- 無線専門の通信事業者は、中国、インド、アフリカにおける3GとLTEの導入が後押しとなり、2016年には通信CAPEX全体のおよそ1/3を占めると予測される。

Infonetics' biannual service provider capex report provides worldwide and regional market size, forecasts, analysis, and trends for revenue and capex by service provider type (incumbent, competitive, cable, and independent wireless) through 2016, and capex by equipment type (CPE, non-telecom/datacom network equipment, and network infrastructure, including broadband aggregation, wireless, IP routers and carrier Ethernet switches, optical, IP voice, TDM voice, video, and all other telecom/datacom network equipment) through 2012.

(原文)

Telecom operators stepping up equipment spending in 2013, led by Asia; growth returns to Europe

Campbell, CALIFORNIA, December 20, 2012-Market research firm Infonetics Research released excerpts from its Service Provider Capex, Revenue, and Capex by Equipment Type report, which tracks telecom operator revenue and capital expenditures (capex) by operator type, region, and equipment segment and provides insight into telecom spending trends.

ANALYST NOTE

"With 3 quarters of the data in and a careful review of carrier investment plans for each major world region, overall telecom service provider capex is on track to be up close to 4% this year led by Asia and North America, and 2013 is looking bright for all regions," says Stephane Teral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

Teral adds: "With investment plans out from AT&T and Deutsche Telekom, combined with the plans of a long list of major and smaller operators around the globe, we can safely say that 2013 and 2014 will be positive capex years, which is good news for vendors. Deutsche Telekom's ?30-billion 3-year investment plan announced this month will help lead a return to investments in the EMEA region. Service providers have no choice but to invest in their networks now; some have been restricting capex for so many years that they are experiencing network outages, unable to handle exploding traffic. There is very high demand for telecom services everywhere, particularly for mobile broadband.

CAPEX REPORT HIGHLIGHTS

- Telecom capex increases in 2012 are being driven primarily by video and wireless infrastructure investments

- Global service provider revenue is on track to reach US$1.9 trillion in 2012, up 4% from 2011

- While incumbent carrier capex on the whole is flat to slightly down this year, independent wireless operators, competitive operators, and cable operators are increasing capex, led by the independent wireless operators, increasing capex 12% this year

- Spending on every type of telecom equipment except optical and TDM voice will be up this year

- The major areas of investment through 2015 include fiber-based wireline broadband, 2G mobile network capacity expansion, 2G migration to 3G, and migration to LTE projects

- Asia Pacific will account for about 1/3 of global service provider revenue by 2016, propelled by China Mobile, the world's largest mobile operator by revenue and subscribers

- Wireless pure-play operators will account for nearly 1/3 of all telecom capex by 2016, driven by 3G and LTE rollouts in China, India, and Africa