アナリストノート

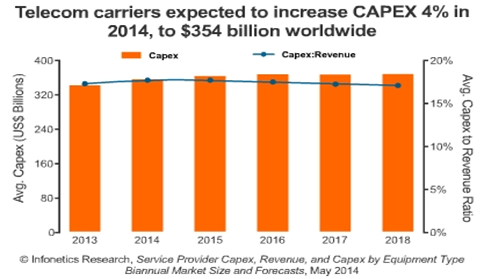

Infonetics Researchでモバイルインフラおよび通信事業者経済面を担当する主席アナリスト、Stéphane Téral氏は次のように報告する。「当社の予測では、この新しい投資サイクルが4年目も続くと、2014年の終わりまでに世界の通信事業の設備投資額が4%上昇して3,540億米ドルに達する見込みです。その投資の大半は、China MobileとChina Telecomが中国で行なう大規模なLTEの展開、およびDeutsche TelekomとVodafoneが欧州全域で行なうネットワークの大規模改修によるものです。」

設備投資レポートのハイライト

アナリストノート

Infonetics Researchでモバイルインフラおよび通信事業者経済面を担当する主席アナリスト、Stéphane Téral氏は次のように報告する。「当社の予測では、この新しい投資サイクルが4年目も続くと、2014年の終わりまでに世界の通信事業の設備投資額が4%上昇して3,540億米ドルに達する見込みです。その投資の大半は、China MobileとChina Telecomが中国で行なう大規模なLTEの展開、およびDeutsche TelekomとVodafoneが欧州全域で行なうネットワークの大規模改修によるものです。」

設備投資レポートのハイライト

- 2013年、数十億の事業者収益および設備投資が米ドル換算で消えてしまった大幅な為替調整の後、世界の通信事業者の設備投資は前年比6.7%成長して3,400億米ドルとなった。

- 日本円が米ドルに対して30%以上下落し、インドルピーは10%の下落、ブラジルレアルは下落し続けている。

- TDM (時分割多重化) 音声、ビデオインフラ、およびCPE (顧客宅内機器) を除くあらゆる種類の設備への支出が2013年には前年比ベースで増加した ― IMS (IPマルチメディアサブシステム) ベースのLTEの展開およびVoLTEへの準備に後押しされVoIP機器は32%上昇した。

- 通信サービスの最前線では、EMEAに牽引される形で、世界での収益が2012年から2013年に1.4%上昇し、1.97兆米ドルとなっている 。

- 世界のあらゆる市場で飽和と競争が激化していく中で、Infoneticsは2013年から2018年にかけての世界の通信サービス収益の成長が、複合年間成長率 (CAGR)1.7%といったゆっくりとしたものになると見ている。

- 通信事業収益への世界第2位の貢献者であるEMEAは、2018年にかけてその先頭ランナーの地位をアジア太平洋地域に脅かされ続けるものと予測されている一方、北米は現状維持、ラテンアメリカは横ばいのままである。

China's huge LTE rollouts and EU network upgrades push carrier capex to $354B this year Campbell, CALIFORNIA, May 15, 2014-Market research firm Infonetics Research released excerpts from its latest Service Provider Capex, Revenue, and Capex by Equipment Type report, which tracks telecom operator revenue and capital expenditures (capex) by operator type, region, and equipment segment and provides insight into telecom spending trends. ANALYST NOTE "As the fourth year of this new investment cycle continues, we're forecasting worldwide telecom capex to rise 4% and hit US$354 billion by the end of 2014, with the bulk of the investment coming from China's massive LTE rollouts led by China Mobile and China Telecom, and from Deutsche Telekom's and Vodafone's major network upgrades across Europe," reports Stéphane Téral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research. CAPEX REPORT HIGHLIGHTS

- In 2013, global telecom carrier capex grew 6.7% year-over-year, to US$340 billion, after a significant forex adjustment that erased billions of operator revenue and capex when converted to the U.S. dollar

- The Japanese yen dropped more than 30% against the U.S. dollar, the Indian rupee dropped 10%, and the Brazilian real continues to drop

- Expenditures for every type of equipment except TDM voice, video infrastructure, and CPE grew on a year-over-year basis in 2013, with IP voice rising 32% powered by IMS-based LTE rollouts and VoLTE preparations

- On the telecom services front, worldwide revenue is up 1.4% in 2013 from 2012, to US$1.97 trillion, dragged by EMEA

- As saturation and competition intensify in every market of the globe, Infonetics projects global telecom services revenue to grow at a slow 1.7% CAGR from 2013 to 2018

- EMEA, the world's #2 telecom revenue contributor, is expected to continue losing ground to frontrunner Asia Pacific through 2018, while North America holds steady and Latin America stays flat