アナリストノート

「集中型RAN (C-RAN)が現実となっているのは、日本と韓国のアジア2か国というきわめて限定された地域です。両国には次の共通点があります。2G不在、高密度、光の普及、イノベーションへの強い志向です」と、Infonetics Researchでモバイルインフラとキャリア経済を担当している主席アナリストであるStéphane Téral氏は述べている。

アナリストノート

「集中型RAN (C-RAN)が現実となっているのは、日本と韓国のアジア2か国というきわめて限定された地域です。両国には次の共通点があります。2G不在、高密度、光の普及、イノベーションへの強い志向です」と、Infonetics Researchでモバイルインフラとキャリア経済を担当している主席アナリストであるStéphane Téral氏は述べている。 「西側諸国で光がC-RAN採用の障害となっているのであれば、無線フロントホールが手を差し伸べてくれるでしょう」としたうえで、「ただ今のところ、これの商用的な採用はみられません。欧州ではOrange、米国ではSprint が主導的な役割を果たしており、両地域でのC-RAN採用は2015年からとみています」と、Téral氏は述べている。

Téral氏はさらに、「C-RANはデフォルト5Gアーキテクチャーとして現れていますが、モバイルネットワークの機能がますます仮想化されるなかで、最終的にはクラウドRANに姿を変えていくでしょう」と続けて述べている。 C-RAN市場のハイライト

- サイトエンジニアリングとアンテナサイトの簡略化によって、少量かつ小型の機器、省電力消費、良好な無線性能、LTEアドバンストへの対応、迅速かつ柔軟性のあるネットワーク空間が実現されている。こうした動きが集中型RAN (C-RAN)の主な促進要因となっている。

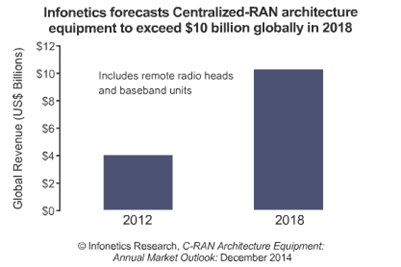

- 世界的なC-RANアーキテクチャー機器の市場は、2012年の40億ドルから2018年までに100億ドルを超える規模になると予測している。その背景には、西側諸国でのRAN拡張のほか、日本と韓国での5Gのロールアウト開始がある。

- ベースバンドユニット(BBU)はアーキテクチャーの中で最も高価な部分であるため、C-RAN全収入の62%を占めている。

- C-RAN市場での上位3ベンダーはアルファベット順に、Ericsson、Nokia Networks、Samsungである。

Infonetics projects C-RAN architecture equipment market to top $10 billion by 2018 Campbell, CALIFORNIA, December 11, 2014-Market research firm Infonetics Research released excerpts from its new C-RAN Architecture Equipment Market Outlook report, which provides market size, share, forecasts, and analysis for centralized RAN (C-RAN) equipment, covering the migration from decomposed to C-RAN architectures including baseband units (BBUs) and remote radio heads (RRHs). ANALYST NOTE "Centralized RAN (C-RAN) is a reality, but very localized in two Asian countries, Japan and South Korea, which share much in common: absence of 2G, high density, fiber ubiquity, and a strong appetite for innovation," notes Stéphane Téral, principal analyst for mobile infrastructure and carrier economics at Infonetics Research.

"If fiber is the barrier to C-RAN adoption in the West, wireless fronthaul is coming to the rescue," Téral. "But we have yet to see commercial deployments. Orange in Europe and Sprint in North America are in the driver's seat, and we expect to see adoption of C-RAN in these regions starting in 2015."

Adds Téral: "C-RAN is emerging as the default 5G architecture and will eventually morph into cloud RAN as more and more mobile network functions are virtualized." C-RAN MARKET HIGHLIGHTS

- Site engineering and antenna site simplification lead to less and smaller equipment, lower power consumption, better radio performance, LTE-Advanced readiness, and agile and flexible network topologies, and these are the chief drivers of centralized RAN (C-RAN)

- The worldwide C-RAN architecture equipment market is forecast to top $10 billion by 2018, up from about $4 billion in 2012, fueled by RAN expansion in the West and the beginning of 5G rollouts in Japan and South Korea

- Baseband units (BBUs) account for 62% of overall C-RAN revenue, as they are the most expensive component of this type of architecture

- The top 3 vendors in the C-RAN market are, in alphabetical order, Ericsson, Nokia Networks, and Samsung