「予想していた通り、LTEのロールアウトはピークに達し、オペレーターが残りのロールアウトを完了していくにつれて四半期あたり収入は60億ドルになっているところです」と、IHSでモバイルインフラとキャリアエコノミクスを担当しているStéphane Téralリサーチディレクターは話している。

モバイルインフラ市場のハイライト

「予想していた通り、LTEのロールアウトはピークに達し、オペレーターが残りのロールアウトを完了していくにつれて四半期あたり収入は60億ドルになっているところです」と、IHSでモバイルインフラとキャリアエコノミクスを担当しているStéphane Téralリサーチディレクターは話している。

モバイルインフラ市場のハイライト

- 世界のLTE収入は2015年第1四半期(1Q15)に前期比1%減の60億ドルになった。

- 1Q15におけるLTEのロールアウトは深刻な減少が続く2G/3Gの落ち込みを相殺するには至らなかった。その結果、世界の2G/3G/4Gモバイルインフラの市場規模は前期比8%減の110億ドルとなった。

- 前年同期比でみると1Q15の2G/3G/4Gモバイルインフラ市場の収入は4%増であった。これは、中国でのTDD LTEの動きが活発であったことによる。

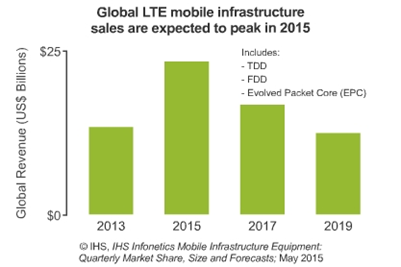

LTE Peaking at $6 Billion a Quarter - Not Enough to Offset 2G/3G Decline Campbell, CALIFORNIA (June 4, 2015)-In its latest IHS Infonetics Mobile Infrastructure Equipment report, IHS (NYSE: IHS) forecasts global LTE mobile infrastructure revenue to peak at $23.3 billion in 2015 and then start to decline as a result of diminishing rollouts. "As we anticipated, we're reaching the peak of LTE rollouts, and LTE is now set to perform at $6 billion a quarter for some time as operators complete their major remaining rollouts," said Stéphane Téral, research director for mobile infrastructure and carrier economics at IHS. MOBILE INFRASTRUCTURE MARKET HIGHLIGHTS

- LTE revenue totaled $6 billion worldwide in the first quarter of 2015 (1Q15), a 1 percent sequential decline

- LTE rollouts were not strong enough in 1Q15 to fully offset the abyssal year-over-year decline of 2G/3G spending, resulting in an 8 percent sequential decline for the global 2G/3G/4G mobile infrastructure market, which came to $11 billion

- On a year-over-year basis, the 2G/3G/4G mobile infrastructure market was up 4 percent in 1Q15, driven by unabated TDD LTE activity in China